How consumer expectation and experience are driving our next normal in branch banking

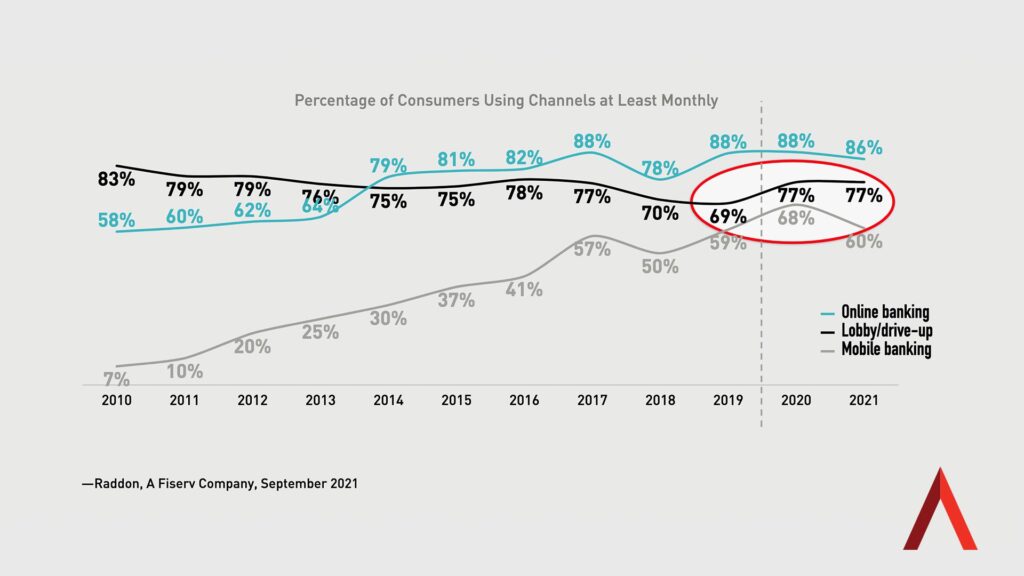

No matter where you look across financial services today, you’ll undoubtedly find news of doom and gloom about the bank branch – including warnings of widespread shuttering of locations across the country. While it’s true that banks continue key closures of branches started during COVID, consumers actually visited branches more during the pandemic, and we’re watching those levels stay steady as we transition to a post-pandemic normal. In fact, Raddon Research reports that 77% people are visiting branches at least monthly, up eight points from 2019, a rate that’s projected to remain after COVID.

Branch Banking Trends

Overall, big banks shut down the largest number of branches in 2021, with Wells Fargo, U.S. Bancorp and Bank of America leading the way in closures. Even Chase, which is known for its branch expansion plans, ranked fourth in closures. On the other hand, community banks shuttered only underperforming branches in metro markets that same year, with 84% of these community institutions not closing a single one of their branches in 2021. Even more, 56% of community banks have reported they’re augmenting their suite of services with additional products, like Wealth Management, and have plans for even more in the coming year.

Yes, an industrywide analysis of FDIC data does project a 3.5% year-over-year decline in physical branches, in tandem with a 3.65% average annual reduction in overall banks, as consolidation continues. But the latest S&P trends data finds U.S. banks are starting to slow the pace of branch network contraction. “If closure activity continued during the remainder of the year at the same pace as in the first six months of 2022, net closures would drop 19% from 2021 levels,” according to the report. This slowdown could very well mark a post-COVID rebalancing in banking, with FIs landing on the ideal mix of digital and physical channels.

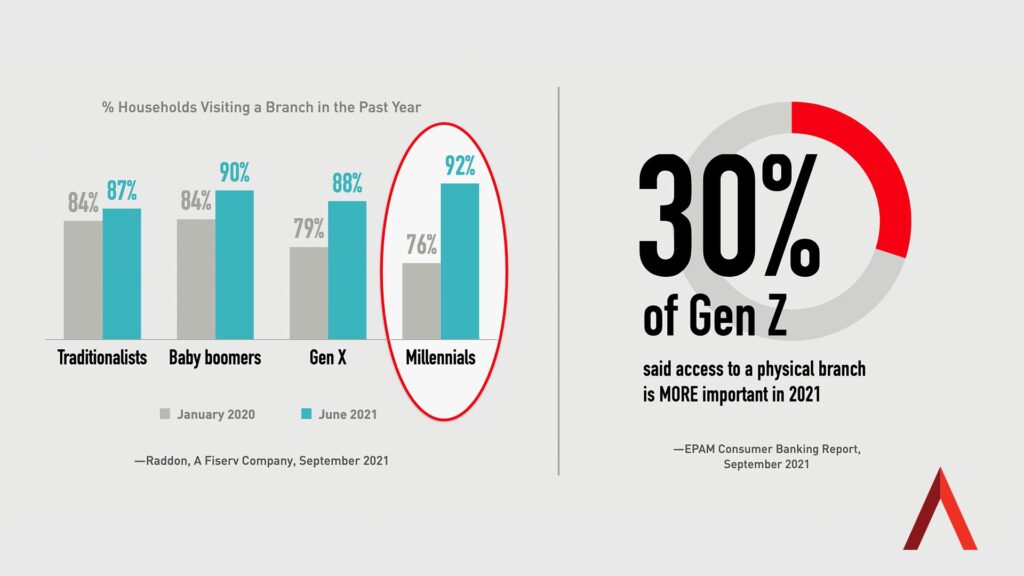

Even as branches close, Morning Consult finds 44% of consumers report they went to their local branch between 1-6 times in June of 2022 alone. For FIs, it may be tempting to assume these branch visits are coming from more traditional, older consumers, and as younger generations become the majority, those branch visits will inevitably wane. However, the reality is that Millennials and Gen Z are key demographic groups driving increases in branch visits, not decreases – with 30% of the youngest banking consumers saying that access to a branch is MORE important than it was before the pandemic.

It’s critical to note that fewer branches doesn’t mean less service. As more branches are closing, each individual branch means more to the consumer and to the financial institution, as well. That’s because what consumers see as the value of the local branch, which is – at its core – consultation and expert advice they will be more likely to act on. “The pandemic has pointed consumers back toward the branches and put pressure on institutions to offer service that is both high-tech and high-touch,” according to Raddon Research, as outlined by Juliet D’Ambrosio in the article, “Smarter Branching for Growth.” She says, ultimately, what consumers want is “both/and: efficient transactions and valuable advice at the point of need.”

Consultation Close-By

The reality of the role branches play as part of banks’ delivery and growth strategies is highly nuanced – and compelling data points to the fact that they remain a hyper-vital delivery channel. As Insider Intelligence notes, ‘‘Contrary to the plethora of predictions proclaiming the end of the bank branch, brick-and-mortar locations remain an important component of the customer experience.” While 90% of US consumers say they’d visit a bank branch for any banking reason, Ipsos finds that 44% of all generations would be most motivated to visit a branch seeking advice, presenting banks with valuable opportunities to deepen relationships.

Further, a compelling McKinsey report presents a counter-narrative to the digital-first story we hear so often. In fact, the industry future McKinsey predicts is both physical and digital where bank branches remain an essential delivery channel – mostly because people will continue to want and need them. In fact, they note a big behavior gap, with consumers reporting they want to bank digitally, but in practice continue to visit branches. “Although willingness to open a new current account digitally hovers around 75%, only 30 to 35% of customers express an actual preference to do so digitally, and only 15% of such accounts are opened digitally.”

The Takeaway

While each financial institution will have to make decisions about market opportunity and branch performance, ultimately, serving customers – nearby, efficiently and with branch experiences they want – remains job #1 for banks. “There’s a new North Star: It’s beautiful and small,” says Gina Bleedorn in her presentation at Future Branches. “Realistically, your full-service branches don’t need to be much more than 2,500 square feet.” And smart FIs are leveraging digital and hybrid technologies to support branch experiences, not supplant them. “Look at an enhanced drive up, a mobile branch on wheels, and an ITM only; these are a North Star strategy, extended across multiple format types and self-service technology.”

For more information on branch banking in our new normal, stay tuned to Believe in Banking’s continuing coverage of the industry’s top trends and topics. For insights on best practices in financial services, including optimizing the branch banking channel for growth, contact the banking and credit union experts at Adrenaline via email at info@adrenalinex.com.